Multinomial Logistic Regression and Machine Learning in R for Economics: End-to-End Simulated Case Studies with EDA

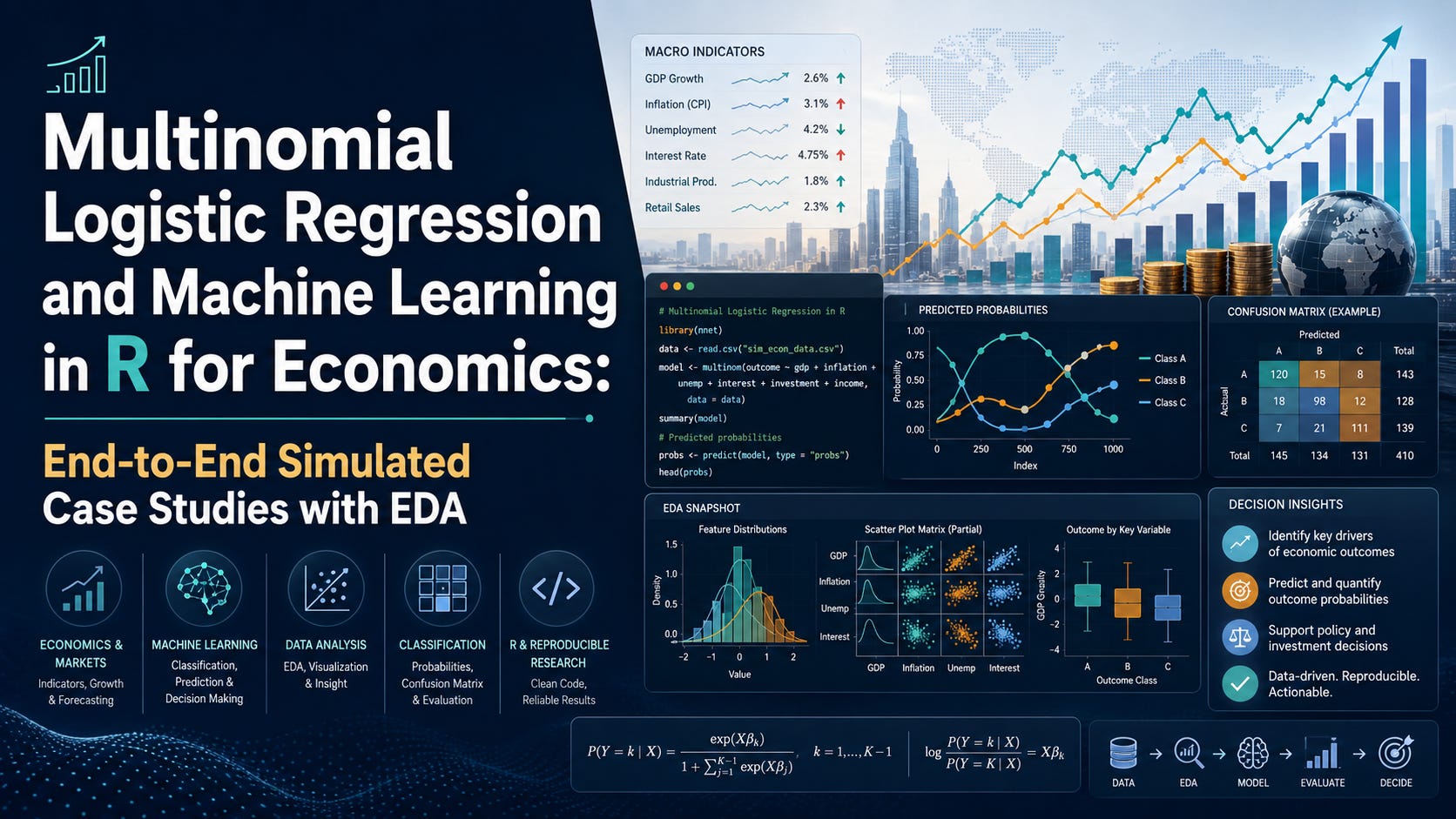

Economic systems do not usually move between simple binary states. An economy may not be merely “good” or “bad”; it may be in recession, slowdown, or expansion. Inflation may be low, near target, or high. Credit markets may be tight, neutral, or loose. These are fundamentally multi-class problems, and they call for models that can estimate the probability of several possible outcomes at once. In that setting, multinomial logistic regression is a natural and powerful extension of the familiar binary logistic model.

What makes multinomial logistic regression especially useful in economics is its combination of interpretability and probabilistic output. It does not just assign a label; it provides a full distribution of probabilities across competing economic states. That is often exactly what economists, policymakers, and financial analysts need. A central bank, for example, may care less about a single hard prediction and more about whether the probability of high inflation has risen from 20% to 45%, or whether recession risk is now materially larger than expansion risk. At the same time, the model’s coefficients remain interpretable, allowing analysts to connect changing class probabilities back to macroeconomic drivers such as the output gap, unemployment, policy rates, yield-curve slope, credit spreads, and financial market conditions.

This guide approaches multinomial logistic regression not as a standalone formula, but as part of a complete machine learning workflow in R. That means beginning with exploratory data analysis (EDA) to understand class balance, variable distributions, and correlation structure; splitting the data into training and test periods in a time-aware way; scaling predictors using training data only; fitting the model; and evaluating it with a rich set of diagnostic tools. Figures such as confusion matrices, one-vs-rest ROC curves, probability density plots, PCA projections, coefficient heatmaps, and rolling accuracy charts help move the analysis beyond a single accuracy number and toward a deeper understanding of model behaviour.

The case studies in this guide—business cycle regimes, inflation states, and credit conditions—are designed to show how multinomial models can be adapted to different kinds of economic questions. Each example uses simulated data so the full workflow can be demonstrated end-to-end, but the underlying logic mirrors real macroeconomic applications. By the end, you will have a transparent and reproducible template for building probability-based multi-class classification models in economics, one that can be extended to real-world datasets, policy scenarios, and financial risk analysis.

This guide shows how to use multinomial logistic regression in R for economic classification problems where the outcome has more than two categories. We will build complete machine learning workflows for three simulated economics case studies:

Business Cycle Regime

RECESSION / SLOWDOWN / EXPANSIONInflation State

LOW / TARGET / HIGHCredit Conditions

TIGHT / NEUTRAL / LOOSE

Each case study includes:

simulated macroeconomic data

feature engineering

EDA

many analytical figures

interpretation of those figures

train/test split

scaling using training data only

multinomial logistic regression using

nnet::multinom()confusion matrix, one-vs-rest ROC curves, probability plots, coefficient heatmaps, and rolling accuracy

At the end, you’ll get a full End-to-End Script (Everything Together).

Become a paid subscriber to access the Analytics Case Studies: complete Python and R scripts, downloadable PDFs, simulated datasets, Shiny app source code, model diagnostics, portfolio projects, and full end-to-end applied analytics workflows.