Multinomial Logistic Regression in Financial Risk Analysis Using Python

A Complete Long-Form Tutorial with Simulated Case Studies, EDA, Interpretation, and End-to-End Script

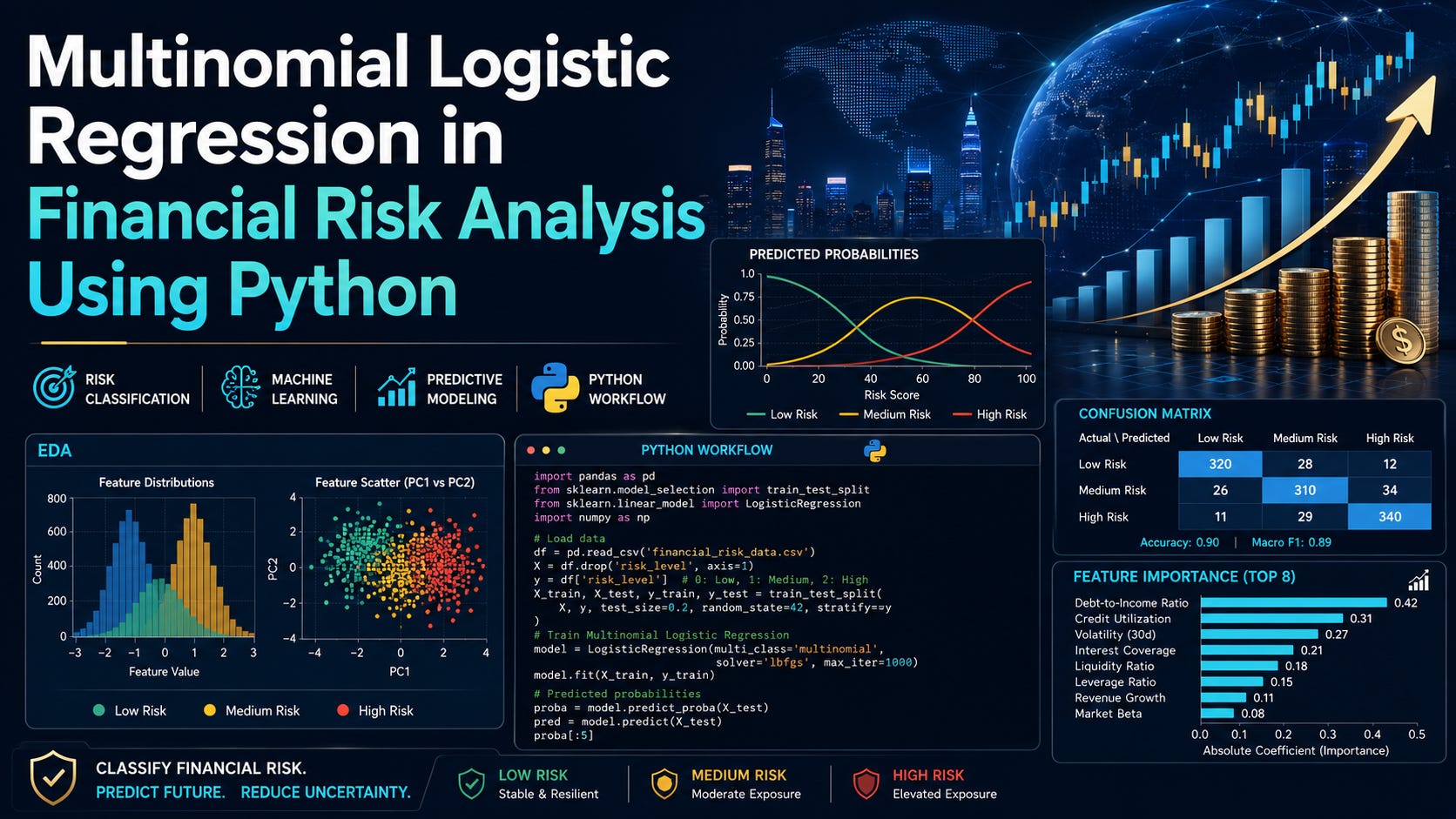

Summary

In financial risk analysis, many of the most important decisions are not binary. A borrower is rarely just “good” or “bad.” A bank’s liquidity condition is not simply “safe” or “unsafe.” A portfolio does not merely “improve” or “deteriorate” in a simplistic two-state world. Real financial systems operate across multiple states of risk, and analysts are often asked to detect, classify, and respond to these states before they become costly.

This is where multinomial logistic regression becomes especially useful. It offers a practical way to model outcomes with three or more categories while still preserving interpretability. In a world where risk managers, credit officers, treasury teams, and portfolio analysts must explain decisions to committees, regulators, and business stakeholders, interpretable models remain extremely valuable. Multinomial logistic regression sits in that sweet spot between statistical rigor and business usability.

In this tutorial, we will build a full end-to-end framework for using multinomial logistic regression in financial risk analysis with Python. Rather than keeping the discussion abstract, we will work through realistic simulated case studies. Each one reflects a common problem in finance: classifying borrower credit risk tiers, identifying liquidity stress states, and monitoring portfolio deterioration. For every case study, we will define the business problem, simulate financially meaningful predictors, conduct exploratory data analysis, fit a multinomial logistic regression model, evaluate its performance, and interpret the results with visual analytics.

The goal is not just to show how the code works. The goal is to show how multinomial logistic regression can be used as a practical decision-support tool in finance. By the end of this guide, you will have a repeatable workflow, multiple case-study templates, a complete end-to-end Python script, and a strong conceptual understanding of how to apply this method in real-world financial risk settings.

Table of Contents

Introduction to Multinomial Logistic Regression in Finance

Why Multi-Class Risk Problems Matter

When to Use Multinomial Logistic Regression

Mathematical Intuition

Python Libraries and Setup

General Modeling Workflow

Case Study 1: Credit Risk Tier Classification

Case Study 2: Liquidity Stress State Classification

Case Study 3: Portfolio Deterioration State Classification

Model Interpretation in Financial Risk Context

Strengths, Limitations, and Practical Considerations

Full End-to-End Python Script

Final Thoughts

1. Introduction to Multinomial Logistic Regression in Finance

Multinomial logistic regression is an extension of binary logistic regression for situations where the dependent variable has more than two categories. In financial risk analysis, that makes it particularly helpful because many important risk outcomes naturally fall into several states.

Examples include:

low, medium, and high borrower risk

normal, stressed, and crisis liquidity conditions

improving, stable, and deteriorating portfolio quality

low, moderate, and severe operational risk events

benign, transitional, and recessionary market regimes

Unlike black-box algorithms that may offer higher predictive performance in some settings, multinomial logistic regression has a major advantage: interpretability. Analysts can directly study how each predictor affects the odds of belonging to one risk class rather than another. This matters in finance, where models often need to be explained and justified.

Another advantage is that the model produces class probabilities, not just class labels. This is important because risk decisions are rarely absolute. A credit officer may want to know that a borrower has a 62% probability of Medium Risk and a 30% probability of High Risk. A treasury team may want to see that a funding shock scenario moves the institution from 10% Crisis probability to 55%. These probabilities are useful for pricing, escalation, provisioning, surveillance, and scenario analysis.

Become a paid subscriber to access the Analytics Case Studies: complete Python and R scripts, downloadable PDFs, simulated datasets, Shiny app source code, model diagnostics, portfolio projects, and full end-to-end applied analytics workflows.